Keywordsconsumer loyalty consumer satisfaction loyalty satisfaction service quality structural equation model

JEL Classification M30

Full Article

1. Introduction

Competition in the banking industry is increasing. Each bank seeks to attract people to become its customers. Programs are designed are aimed at diversifying the product, providing a variety of facilities and promising rewards. This effort to prevent migration of customers to other brands and creating customer satisfaction and making customers remain loyal to the brand of banking. In conditions of high competition, the main thing that should be prioritized is to create customer satisfaction and maintain customer loyalty.

PT. Bank Negara Indonesia (Persero) Tbk is one of the state banks that serve customers well. BNI regard customers as an important asset in the banking system. BNI implementing service quality strategy with the overriding goal of profit and can survive in a competitive competition. The products offered are very diverse and are aimed to reach various groups of customers. There are several phenomena that arise in carrying out banking activities such as the lack of response to the BNI to customers. It can be seen from at least checkout counter that operates to serve customers so that customers have to queue for a long time. ATM physical facility that is still less effective and the cleanliness of the physical facilities are not maintained. This becomes a disappointment for customers. It can also be seen in the level of development of the number of customers during 2009 to 2013 in the province of Aceh.

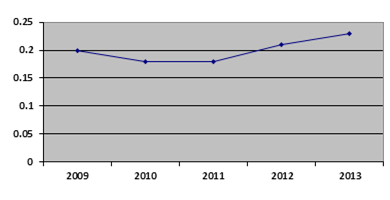

Figure 1. Evolution of customer number between 2009 and 2013

Source: PT. BNI (Persero) Tbk Aceh Province, Indonesia

In 2009 the number of customers of BNI in the Aceh province was 87,349 persons (20 percent) of the total over five years. In 2010, it decreased to 81,385 persons (18 percent). In 2011, it increased slightly as many as 82,770 persons (18 percent). Meanwhile, in 2012 it has increased sharply to 94,561 persons (by 21 percent). Finally In 2013, it has increased again to many as 101,238 persons (by 23 percent).

Maintaining customer loyalty is the strategic policy for banking companies because it is part of the company's strategy in the face of competitors and connects companies to the markets. Customer loyalty is needed as an element in a competitive marketing strategy. The success of today’s businesses has become the most important strategic goal because the loyal customers can increase revenues.

There are few studies that are relevant to this study as, Maiyaki and sanuri (2012) found that the technical quality, the value and image of the banking retail have a positive influence on the intention to behave in Nigeria. While functional quality does not have a significant relationship with the actual behavior of customers. Siddiqi (2011) says that the quality of service, corporate image and customer value is positively related to customer loyalty in the banking retail sector in Bangladesh. In Malaysia, Munusamy et al. (2010) says that the tangibles have a significant influence on customer satisfaction while assurance, reliability, empathy and responsiveness have no effect on customer satisfaction. Gan et al. (2006) in New Zealand examined the retention of customers in the banking industry. The results showed that: (1) Satisfaction and image have a positive influence on the value. (2) Satisfaction and Value have a positive influence on the intention. (3) Competitive, satisfaction, value, image, the challenge have a positive influence on loyalty (4) Intention and loyalty have a positive influence retention.

Local research specifically on Bank BNI in Indonesia, conducted by Yusmahdi (2013) says that there is significant influence of service quality on customer trust and loyalty while the quality of service did not affect to customer satisfaction. Putra (2012) found that service quality did not affect significant and positive on loyalty of credit borrowers at BNI branch office SKC Malang. The study of Octariani (2008) found that there is a strong and positive relationship between quality of service and satisfaction to customer loyalty. Triyatati (2001) say that the value of the product, the value of service and value of employee and customer satisfaction have is a significant and strong relationship. Bachri et al. (2016) says that the credibility, customer value, satisfaction and loyalty are an important element in improving the performance of banks in Indonesia.

From some research above, there is a gap that can still be researched and contributed to with theoretical perspectives. The authors use the variables quality of service, satisfaction and loyalty of customers at several main branches in the Aceh Province. The variable of quality of services undertaken by previous researchers still do not provide maximum results, meaning that there is no significant effect on results between service quality on customer satisfaction and loyalty (Yusmahdi, 2013; Maiyaki and Sanuri, 2012; Munusamy et at., 2010; Gan et al., 2006).

This research aims to look at the impact of service quality on customer satisfaction and its implication to customer loyalty at PT. BNI Persero in Aceh Province, Indonesia.

2. Literature Review

2.1. Service Quality

Gaspersz (2002) defines quality as the totality of characteristics of a product and services that support the ability to meet specified requirements. Quality is often defined as everything that satisfies customers or conformity to the requirements or needs. Lupiyoadi and Hamdani (2011) say that the service quality has the important essence for the company's strategy to defend them and achieve success in the face of competition.

Parasuraman et al. (1994) stated that the SERVQUAL measurement has more diagnostics and more practical implications to assess the customer perception of service quality for a variety of service industries. The five dimensions of service quality include: (1) tangibles (appearance of physical components); (2) reliability (dependability of service provider and accuracy of performance); (3) responsiveness (promptness and helpfulness); (4) assurance (knowledge and courtesy of employees and their ability to inspire trust and confidence); and (5) empathy (caring, individualized attention the firm gives its customers).

2.2. Satisfaction

Kotler (2003) defines satisfaction as the feeling of being happy or disappointed as experienced after comparing the perception of performance or the result of a product with expectations. Customer expectations are formed and were based on several factors, including the shopping experience in the past, the opinion of friends and relatives, as well as information and Promises Company and its competitors. Satisfaction can be interpreted as an effort to fulfill something or make something adequate (Tjiptono, 2005). Rangkuti (2004) explains that the meaning of customer satisfaction i.e., the difference between the rate of interest and perceived performance or results.

Oliver (1980) explained that customer satisfaction entails the full meeting of customer expectation of the products and services. If the perceived performance matches or even exceeds customers’ expectations of services, they are satisfied. In the real world, unsatisfied customers tends to create negative word-of-mouth and convey their negative impression to other customers (Newman, 2001). Lupiyoadi and Hamdani (2011) says that the benefits received from measuring customer satisfaction is to increase customer loyalty, prevent rotation / movement of customers, reduce price sensitivity, reduce the cost of marketing failures and operating costs, improve advertising effectiveness and improve business reputation.

Kotler and Keller (2007) says that consumers want to buy a product with the hope will provide benefits when used which is divided into three categories: performance or benefits of the product that has been purchased and employed, compared with expectations, and the results of the assessment, which is divided into three categories namely, (1) positive disconfirmation, when performance exceeded expectations yield high satisfaction responses and will come back to repurchase. (2) Simple disconfirmation, where performance in line with expectations implies a neutral response and affects the desire to repurchase. (3) The negative disconfirmation, when performance is lower than expectations so there is no desire back to repurchase.

2.3 Loyalty

Loyalty is the attitude of the customer to make his choice to keep using a product or service from a company. Attitude determines the selection and also to make a commitment to repurchase the company's (Foster and Cadogan, 2000). According to Wulf et al. (2001) loyalty is the amount of consumer loyalty and frequency of purchases made by a customer of a company. The authors managed to find that the quality of integration consisting of satisfaction, trust and commitment has a positive relationship with loyalty. Lamb et al. (2004) investigated the relationship between the received satisfactions and customer loyalty. Results achieved an important justification as the reference that the relationship of customer satisfaction, with customer loyalty is positive.

According to Oliver (1997), the variable of fidelity has four dimensions, among others:

1. Cognitive loyalty is about the perceptions about the ability to assess the bank at a glance with the following indicators: (a) Knowing that when selecting and assessing a bank is a fetching the right decision. (b) Assess that the ability of the selected bank is the best.

2. Affective loyalty implies the customer perception regarding the election to use the bank with the following indicators: (a) Using the services and facilities provided. (b) Liking all the activities provided.

3. Conative loyalty represents the perception of consumers regarding the action to continue using the bank with the following indicators: (a) Always stay would choose a bank. (b) The repurchase.

4. Action loyalty represents the opinion of the customers on the action to continue using the bank with a higher commitment with the following indicators: (a) Provide positive information to others. (b) No change in other banks.

2.4 Relationship Between Variables and Hypotheses

Patel and Pithadia (2013) say that quality perception is an important factor that gives influence on customer satisfaction at selected banks in Mehsana District Gujarat. Octariani (2008) says that there is a strong and positive relationship between service quality and satisfaction on customer loyalty. Munusamy et al. (2010) adds that service quality has a significant and positive impact on customer satisfaction. While Yusmahdi (2013) stated that the quality of service does not provide a positive and significant impact on customer satisfaction. The hypothesis that can be submitted is:

H1: There is influence of service quality on customer satisfaction at PT. BNI (Persero) Tbk. In Aceh Province.

Putra (2013) finds that the quality of services has a significant and positive influence on customer loyalty in commercial banks in Malang. Auka (2012) adds that simultaneously the quality of service, customer value and customer satisfaction affect customer loyalty in commercial banking in Kenya. Ishaq (2012) argued that the quality of service and customer value significantly affect customer loyalty to the telecommunications industry of Pakistan. Siddiqi and Omar (2011) prove that service quality and customer loyalty are positively related to retail banking in Bangladesh. While Alireza et al. (2012) find that service quality has no significant effect on customer loyalty to telecommunication companies in Iran. Similarly Maiyaki and Sanuri (2012) state that functional quality has no significant effect on customer behavior intention in retail banking in Nigeria. Hypotheses that can be submitted are:

H2: There is influence of service quality to customer loyalty at PT. BNI (Persero) Tbk. In Aceh Province.

According to Calik and Balta (2006) states that customer satisfaction and loyalty is the effect of receiving the quality of service performed by an organization. Suhartanto (2001) finds that customer satisfaction will affect consumer behavior to recommend others, encourage friends or friends to, do business with, consider as an option, first if you want to buy similar services, buy services in the future and inform the good things from to others. Hypotheses that can be submitted are:

H3: There is influence of customer satisfaction to customer loyalty at PT. BNI (Persero) Tbk. In Aceh Province.

3. Methodology

The aim of this study is to understand the influence of service quality toward customer satisfaction and its implication on customer loyalty at PT. BNI (Persero) Aceh Province. The cluster and convenience sampling technique were used for this study. Respondents were customers visiting the counters of banks and they must have an account with PT. BNI (Persero) operating all branches in Aceh, namely the branches of Banda Aceh, Lhokseumawe, Sigli, Bireuen, Meulaboh, and Langsa. The data were collected from personal interviews using questionnaires.

A five-point Likert scale was used to measure customer perceptions of service quality, customer satisfaction, and customer loyalty, ranging from “strongly disagree” (1) to “strongly agree” (5). Service quality was measured by adapting and modifying indicators as suggested by Parasuraman et al. (1994); customer satisfaction and loyalty adapting and modifying indicators indicators from Oliver (1997).

4. Analysis and Results

4.1 Respondents’ Profile

Table 1 reports the descriptive statistics of respondents in this study. A total of 250 questioners were distributed and 210 were returned (84 percent response rate). The characteristic includes 119 male customers (56.7 percent) and 91 female customers (43.3 percent). The dominantly respondents age is 21 – 30 years (33 percent) and works as Government employee (33.8 percent).

Table 1. Respondents' profile

| Frequency | Percent | Cumulative Percent | |

| Gender | |||

| Male | 119 | 56.7 | 56.7 |

| Female | 91 | 43.3 | 100.0 |

| Age (year) | |||

| 17-20 | 20 | 9.0 | 9.0 |

| 21-30 | 69 | 33.0 | 42.0 |

| 31-40 | 53 | 25.0 | 67.0 |

| 41-50 | 56 | 27.0 | 94.0 |

| 50 and above | 12 | 6.0 | 100.0 |

| Occupation | |||

| Lecturer/Teacher | 20 | 9.5 | 9.5 |

| Private employee | 32 | 15.2 | 24.7 |

| Government employee | 71 | 33.8 | 58.5 |

| Businessman | 40 | 19.0 | 77.5 |

| Student | 27 | 12.9 | 90.4 |

| Other | 20 | 9.6 | 100.0 |

| Marital Status | |||

| Married | 144 | 83.2 | 83.2 |

| Single | 29 | 16.8 | 100.0 |

| Education | |||

| High School | 20 | 11.6 | 11.6 |

| Undergraduate | 46 | 26.6 | 38.2 |

| Graduate | 87 | 50.3 | 88.4 |

| Postgraduate | 20 | 11.6 | 100.0 |

Source: SPSS Output, 2016

4.2 Structural Equation Model (SEM) Analysis

Confirmatory Factor Analysis

Confirmatory Factor Analysis test is conducted with a purpose to know the ability level of an instrument or tool for collecting data by expressing main target of measurement. The CFA test in this research is divided into two types, namely exogenous constructs and endogenous constructs. There is one exogenous variable, namely service quality consisting of five dimensions, namely tangible, empathy, reliability, responsiveness and assurance.

The tangible dimension consists of five indicators but, after being analysed, it has only four indicators forming the dimension. The empathy dimension consists of nine indicators, but after being analysed it has only seven forming indicators. The reliability dimension has seven indicators, but after being analysed it has only four forming indicators. The responsiveness dimension has four indicators, after being analysed it has only four forming indicators. Finally, the assurance dimension has six indicators, but after being analysed it has only five forming indicators.

The endogenous construct in this research consists of two variables, namely customer satisfaction and customer loyalty. The satisfaction has four valid indicators. The loyalty has seven indicators but after being analysed it has only five forming indicators.

Measurement Model

The measurement model test is conducted to know the accuracy on manifest variable so that it can describe on latent variable (Santoso, 2011). In this research, it is conducted the measurement model test on exogenous construct and endogenous construct. The Measurement model for the exogenous constructs covariance tangible, empathy, reliability, responsiveness and assurance. From the analysis, it shows that the model has met the requirements. The first and second order analyses are also conducted; the first order shows that all of forming indicators have had ideal loading factors so that for the first order, it has met the criteria. Also for the second order, all of the forming indicators have had loading factor value to meet the criteria. Meanwhile the Measurement model for endogenous constructs covariance the customer satisfaction and loyalty variables. From some Goodness of Fit Test criteria, these show GFI, AGFI, TLI, CFI, RMSEA, CMIN and P-Value values to meet the requirements for model properness. However the exogenous and endogenous constructs can be united in the following analysis.

Structural Model

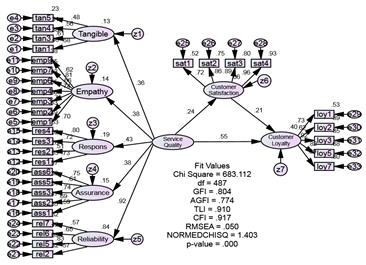

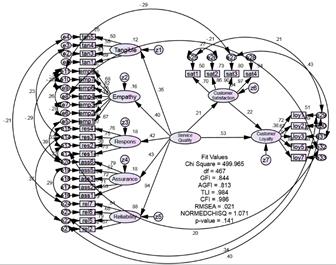

The testing of the structural model is conducted in two stages. The first stage implies exploring the extent of the formed basic model in this research to meet the goodness of fit criteria so that the model can describe on the research phenomena. The second stage shows the ideal model through modification indices. Both models can be seen in figures 2 and 3, and tables 2 and 3.

Figure 2. SEM results for Basic Model

Table 2. SEM results for Basic Model

| Criteria | Cut off | Results |

| Chi square | p>0.05 | 683.112 |

| Goodness of fit index (GFI) | >0.90 | 0.808 |

| Adjusted Goodness of fit index (AGFI) | >0.90 | 0.774 |

| Tucker Lewis Index (TLI) | >0.95 | 0.910 |

| Comparative Fit Index (CFI) | >0.95 | 0.917 |

| Root Mean Square Error of Approximation (RMSEA) | <0.08 | 0.050 |

| CMIN | <= 2 | 1.43 |

| P-value | > 0.05 | 0.000 |

Figure 2. SEM results for the Model with Modification Indices

Table 3. SEM results for the Model with Modification Indices

| Criteria | Cut off | Results | Conclusion |

| Chi square | p>0.05 | 499.965 | Good |

| Goodness of fit index (GFI) | >0.90 | 0.844 | Marginal |

| Adjusted Goodness of fit index (AGFI) | >0.90 | 0.813 | Marginal |

| Tucker Lewis Index (TLI) | >0.95 | 0.984 | Good |

| Comparative Fit Index (CFI) | >0.95 | 0.986 | Good |

| Root Mean Square Error of Approximation (RMSEA) | <0.08 | 0.021 | Good |

| CMIN | <= 2 | 1.71 | Good |

| P-value | > 0.05 | 0.141 | Good |

The basic model has yet to meet the criteria of model properness, among others from the GFI, AGFI, TLI, CFI and P-Value values. There are only a good criteria in Chi Square, RMSEA and CMIN. This model can yet represent the phenomena in banking industry in Aceh Province. The second model is the modification indices, this model shows that the criteria have meet although there are two requirements with marginal values, (rather good), namely GFI and AGFI. The CMIN and P-Value values are the main requirements that have to be met in this model.

Estimation on Parameter Values

Estimations on parameter values aim to show the amount of coefficient value of a variable. This coefficient value is also used for the hypotheses testing that have been formulated. To see the amount of coefficient value of each variable, it is used to estimate standardized regression weights such as seen in the following table (Table 4).

Table 4. Estimation on Parameter Values

| Examined relationship | Estimate Unstandardized | Estimate Standardized | S.E. | C.R. | P | ||

| Responsiveness | <--- | Service Quality | .793 | .425 | .233 | 3.401 | *** |

| Tangible | <--- | Service Quality | .642 | .346 | .233 | 2.760 | .006 |

| Assurance | <--- | Service Quality | .557 | .427 | .174 | 3.194 | .001 |

| Reliability | <--- | Service Quality | 1.000 | .940 | |||

| Empathy | <--- | Service Quality | .634 | .404 | .187 | 3.398 | *** |

| Satisfaction | <--- | Service Quality | .244 | .205 | .118 | 2.058 | .040 |

| Loyalty | <--- | Service Quality | .681 | .530 | .163 | 4.188 | *** |

| Loyalty | <--- | Satisfaction | .241 | .223 | .083 | 2.913 | .004 |

Source: Amos Output, 2016

Estimation value of service quality on the customer satisfaction is 0.205 with a significance of 0.040, that is smaller than α = 0.05. The Critical Ratio (CR) value is 2.058 which is greater than Z = 1.96. This means that the service quality significantly and positively affects the customer satisfaction at PT. BNI (Persero) Tbk. in Aceh Province.

The estimation value of service quality on the customer loyalty is 0.530 with a significance of 0,000 which is smaller than α = 0.05. The Critical Ratio (CR) value is 4.188 which is greater than Z = 1.96. This means that the service quality significantly and positively affects the customer loyalty at PT. BNI (Persero) Tbk. in Aceh Province.

Estimation value of customer satisfaction on the customer loyalty is 0.223 with a significance of 0.004 which is smaller than α = 0.05. The Critical Ratio (CR) value is 2.913 which is greater than Z = 1.96. This means that the customer satisfaction significantly and positively affects the customer loyalty at PT. BNI (Persero) Tbk. in Aceh Province.

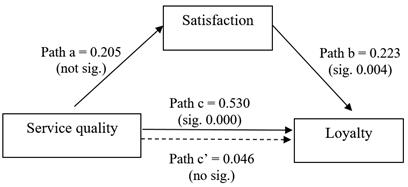

Testing the Mediator Variable

The mediator variable model is introduced by Baron and Kenny (1986). Baron and Kenny described the procedure of mediated variable analysis in a simple manner through regression. The analysis path in this research can be seen in the following figure.

Figure 4. Mediated Model for this research

Based on figure 4 above, it can be described that path a significantly affects customer satisfaction. Path c significantly affects loyalty, but the path c’ does not significantly affect loyalty. This path correlation is based on the opinion by Baron and Kenny (1986), so it can be concluded that the customer satisfaction variable can serve as a partial mediator variable between service quality on loyalty at PT. BNI (Persero) Tbk. in Aceh Province.

5. Conclusion

5.1. Research Implications

These research results can provide various implication, both theoretically and practically. The research results obtained show positive and significant effects of service quality on customer satisfaction and customer loyalty, and customer satisfaction can partially mediate the relationship between service quality and customer loyalty for PT. BNI (Persero) Tbk Aceh Province. Based on the theory expressed by Parasuraman et al. (1994); Lupiyoadi and Hamdani (2011) said that the quality of service has an essential importance for the company's strategy to defend itself and achieve success in the face of competition.

Patel and Pithadia (2013) say that the perception of quality is an important factor that gives a positive effect on customer satisfaction on selected banks. Auka (2012) adds that service quality and customer satisfaction can improve and maintain customer loyalty in commercial banking. Suhartanto (2001) says that customer satisfaction will affect consumer behavior to recommend others.

This research also proves the theory stating that service quality is essential in improving customer satisfaction and loyalty directly or indirectly. These research results show that PT. BNI (Persero) Tbk in Aceh Province has good service quality. Its implication is that PT. BNI (Persero) Tbk must maintain and improve its service quality in order to improve customer satisfaction and loyalty directly or indirectly. High customer satisfaction can imply that customer loyalty directly improves the growth and profit of PT. BNI (Persero) Tbk in Aceh Province.

5.2. Conclusion

PT. BNI (Persero) Tbk in Aceh Province have good service quality. This good service quality can improve customer satisfaction in getting bank services. Good service quality and high customer satisfaction can improve customer loyalty on the banking products, services and company in Aceh Province. The service quality variable with five dimensions, namely tangible, empathy, responsiveness, reliability and assurance affects significantly and positively on the customer satisfaction by bank customers in Aceh Province. This is consistent to Patel and Pithadia (2013) stating that service quality has positive correlation with customer satisfaction. Than service quality has significant and positive effect on customer loyalty (Siddiqi, 2011; Gan et al., 2006). The customer satisfaction can mediate appropriately the correlation of service quality and customer loyalty. This research is consistent to a research by Octariani (2008) stating that customer satisfaction can be as mediator variable between service quality and customer loyalty.

5.3. Recommendation

Although there is a good service quality provided by the banks in Aceh province, as perceived by their customers, it is necessary for companies to keep maintaining and improving the service quality, mainly in empathy dimension by improving employees’ knowledge and capability. Meanwhile to improve the credibility, it can be by providing training and education concerning sharia product and service comprehension so that it can improve customer satisfaction. Although there is high customer satisfaction banks in Aceh Province, the bank party should keep maintaining the commitment by creating Internet Information technology application that can be accessed easily for banking transactions. The use of this information technology innovation can improve duration of correlation between the banking and customers. To maintain and improve customer loyalty, companies should update and utilize their facilities optimally to prevent any disappointment in providing services and improve repeated purchase on products and services in Aceh Province.

References

- Auka, D.O., 2012. Service Quality, Satisfaction, Perceived Value and Loyalty Among Customers in Commercial Banking in Nakuru Municipality, Kenya. African Journal of Marketing Management, Vol. 4(5), pp. 185-203.

- Bachri, N., Rahman Lubis, A., Nurdasila and Abd. Majid, M.S., (2016. Credibility and Consumer Behavior of Islamic Bank in Indonesia: A Literature Review. Expert Journal of Marketing, 4(1), pp. 20-23.

- Cengiz, E., Ayyildiz, H., and Buyamin, 2007. Effects of Image and Advertising Efficiency on Customer Loyalty and Antecedents of Loyalty: Turkish Banks Sample. Banks and Bank Systems. 2(1).

- Deng, Z., Lu, Y., Wei, K.K., and Zhang, J., 2010. Understanding Customer Satisfaction and Loyalty: An Empirical Study of Mobile Instant Messages in China. International Journal of Information Management, 30, pp. 289-300.

- Gan, C., Cohen, D., Clemes, M., and Chong, E., 2006. A Survey of Customer Retention in the New Zealand Banking Industry. Banks and Bank Systems, 1(4), pp.83-99.

- Ishaq, M.I., 2012. Perceived Value, Service Quality, Corporate Image and Customer Loyalty: Empirical Assessment from Pakistan. Serbian Journal of Management, 7 (1), pp. 25-36.

- Kotler, P., 1997. Marketing Management: Analysis, Planning, Implementation and Control. 9th edition. New Jersey: Prentice Hall International.

- Kotler, P., 2007. Marketing Management. Edisi Ke Sebelas, Jakarta: Jilid 2, PT. INDEKS.

- Kotler, P., and Amstrong G., 2000. Prinsip-prinsip Pemasaran. Jakarta: Penerbit Erlangga.

- Kotler, P., and Keller, K.L., 2007. Manajemen Pemasaran. Edisi Bahasa Indonesia: Penerbit Indeks.

- Kotler, P., Keller, K.L., Ang, S.H., Leong, S.M., and Tan, C.T., 2006. Marketing Management: An Asian Perspective. Singapore: Pearson Prentice Hall.

- Maiyaki, A. A. and Sanuri, S. M. Mokhtar (2012. Determinants of Customer Behavioural Responses in the Nigerian Retail Banks: Structural Equation Modeling Approach. African Journal of Business Management, 6(4), pp. 1652-1659.

- Munusamy, J., Chelliah, S., and Mun, H. W., 2010. Service Quality Delivery and Its Impact on Customer Satisfaction in the Banking Sector in Malaysia. International Journal of Innovation, Management and Technology, 1(4), pp.398-404.

- O’Cass, A., and Fenech, T., 2003. Webretailing Adoption: Exploring the Nature of Internet Users Webretailing Behaviour. Journal of Retailing and Consumer Services, 10, pp.81-94.

- Octariani, E.N., 2008. The Analysis of Influence between service quality and satisfaction toward customer loyalty (Case Study at PT. BNI (Persero) Tbk. Thesis, Islamic State University: Syarif Hidayatullah Jakara.

- Oliver, R.L., 1999. Where Common Loyalty?. Journal of Marketing. 63, pp. 33-44.

- Parasuraman, A., Zeithaml, V., A., and Berry, L.L, 1988. SERVQUAL: A Multiple Item Scale for Measuring Consumer Perceptions of Service Quality. Journal of Retailing, 64(1), pp.12-40.

- Patel, H. and Pithadia, V., 2013. Emerging Trends in Customer Satisfaction of Value Added Services in Selected Banks at Mehsana District of Gujarat. International Monthly Refereed Journal of Research in Management and Technology, Vol. II, pp.9-15.

- Putra, I.W.J.A., 2012. Pengaruh Kualitas Pelayanan Terhadap Loyalitas Debitur Kredit Produktif (Studi pada Kantor Cabang BNI SKC Malang. Jurnal Aplikasi Manajemen, 10(2).

- Putra, I.W.J.A., 2013. The Effect of Quality and Service Value on Customer Loyalty (A Study on the Customers of Commercial Banks in Malang City. Interdisciplinary Journal of Contemporary Research in Business, 5(5), pp.488-504.

- Rangkuti, F., 2008. Measuring Customer Satisfaction. Jakarta: Penerbit Gramedia Pustaka Utama.

- Razavi, S.M., Safari, H., Shafie, H., and Khoram, K., 2012. Relationship Among Service Quality, Customer Satisfaction and Customer Perceived Value: Evidence from Iran’s Software Industry. Journal of Management and Strategy, 3(3), pp.28-37.

- Siddiqi, K.O., 2011. The Drivers of Customer Loyalty to Retail Banks: An Empirical Study in Bangladesh. Industrial Engineering Letters, 1(1), pp.40-55.

- Sugiyono, 2002. Metode Penelitian Bisnis. Bandung: Penerbit CV. Alfabeta.

- Tjiptono, F., 1997. Manajemen Jasa. Yogyakarta: Penerbit Andi Offset.

- Tjiptono, F., 2006. Pemasaran Jasa. Edisi Pertama, Malang: Bayumedia Publising.

- Triyatati, A., 2001. Analisis Tanggapan dan Kepuasan Nasabah Tabungan plus Utama Bank BNI Sebagai Dasar Menyusun Strategi Pemasaran (Studi Kasus pada PT. BNI (persero) Tbk Kantor Cabang Semarang. Publikasi Thesis, Universitas Diponegoro Semarang.

- Yusmahdi, 2013. Pengaruh Kualitas Pelayanan Terhadap Loyalitas Dengan Kepuasan dan Kepercayaan Nasabah Sebagai Variabel Intervening Pada Nasabah PT. BNI Cabang Lhokseumawe. Publikasi Tesis, Universitas Malikussaleh.

Article Rights and License

© 2017 The Authors. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.